Customer Data Platforms (CDPs) are revolutionizing how data-driven marketers manage and leverage customer information. At their core, CDPs ingest customer data from various source systems, unify it into a single, comprehensive customer database, and make it readily available for use across other integrated systems.

CDPs were initially designed to be primarily managed by marketing departments, significantly reducing the reliance on IT support. This accessibility and power explain the growing buzz around these platforms. To understand the current landscape, we delve into recent market research on the CDP industry in Europe, published by the Customer Data Platform Institute.

European CDP Market Growth and Local Vendors

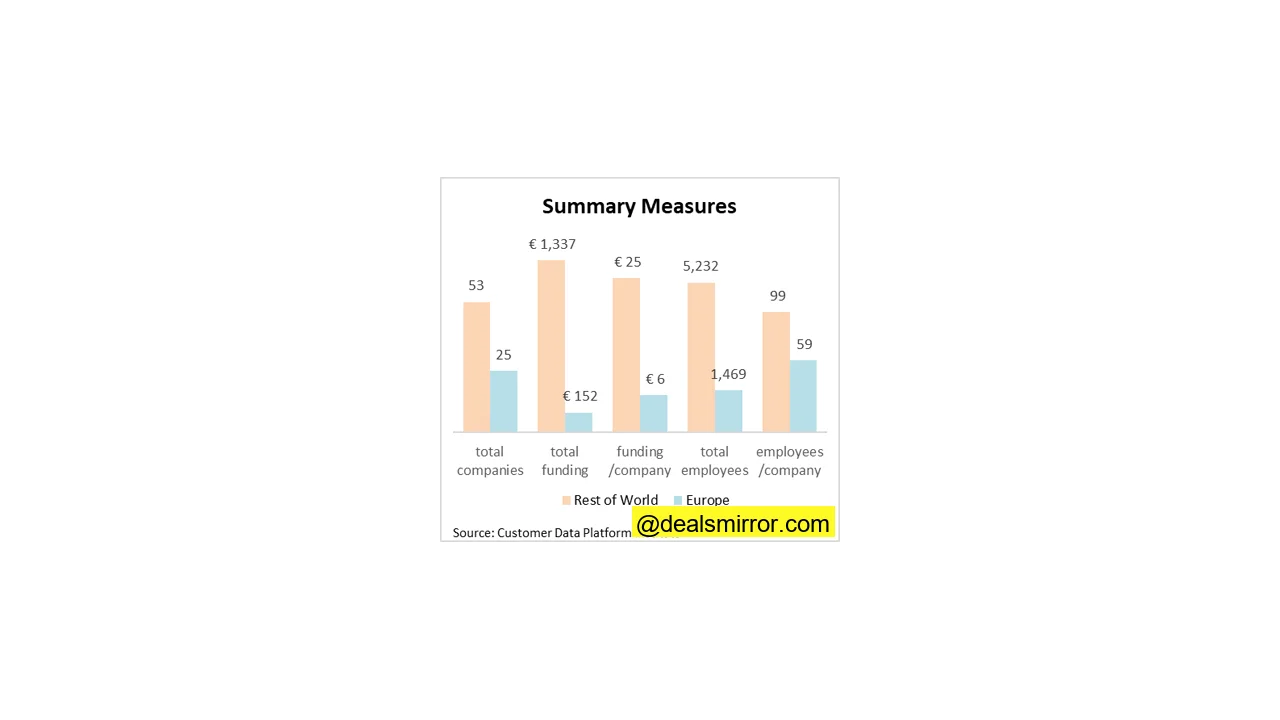

For buyers, a key takeaway from the EU CDP industry report is the significant number of local vendors. Europe is home to 25 CDP vendors, accounting for nearly one-third of the global total. This means marketers in countries like the UK, France, or The Netherlands have a choice of roughly half a dozen domestic providers.

This local presence is crucial due to enduring national market differences. Many buyers often prefer to collaborate with local firms, especially for customer-facing applications like personalization, where a deep understanding of local consumer behavior is paramount.

The market also exhibits impressive growth:

- The number of European vendors doubled in 2018, growing from 13 to 25.

- Cumulative funding for these vendors increased by a modest 16%, suggesting that much of this growth is self-funded.

The total revenue generated by these Europe-based vendors was estimated at €150 million in 2018, with revenue from non-European vendors in Europe likely matching this figure.

Understanding the Different CDP Types

The report differentiates CDPs into three main categories, each with an incremental scope regarding data access, analytics, and campaign capabilities. It’s important to note that significant variations exist even among vendors within the same category.

- Data Access CDPs: These systems focus on collecting customer data from various sources, linking it to individual customer identities, and storing it in a persistent database that is accessible to external systems. They represent the foundational set of functions for a CDP, often utilizing specialized data management technologies. Many originated as tag management or web analytics providers.

- Analytics CDPs: Building upon data assembly, these systems integrate analytical applications. Common features include customer segmentation, with some extending to machine learning, predictive modeling, revenue attribution, and customer journey mapping. They frequently automate the distribution of segmented lists to marketing automation or advanced analytics platforms.

- Campaign CDPs: These are the most comprehensive, offering data assembly, analytics, and direct customer treatment capabilities. Such treatments can encompass personalized messages, real-time interactions, product or content recommendations, outbound marketing campaigns, and customer journey orchestration. What distinguishes them is their ability to also specify the message or action to be delivered.

Below is a comprehensive list of the European CDP vendors featured in the report, categorized by their country of origin and CDP type:

| CDP Name | Country | Category |

|---|---|---|

| Advalo | France | campaign |

| Audiens | Netherlands | analytics |

| BlueVenn | UK | campaign |

| Boxever | Ireland | campaign |

| Camp de Bases | France | campaign |

| Celebrus | UK | access |

| CommandersAct | France | access |

| ContactLab | Italy | campaign |

| CrossEngage | Germany | campaign |

| Datatrics | Netherlands | campaign |

| Eulerian | France | analytics |

| Fospha | UK | campaign |

| IntentHQ | UK | campaign |

| Invicta | Netherlands | campaign |

| Jahia / Unomi | Switzerland | campaign |

| LeadBoxer | Netherlands | analytics |

| NGDATA | Belgium | analytics |

| Nominow | Netherlands | campaign |

| Omnisient | South Africa | access |

| Piwik Pro | Poland | campaign |

| PRDCT | Netherlands | analytics |

| RedEye | UK | campaign |

| Splio | France | campaign |

| UniFida | UK | campaign |

| Ysance | France | access |

CDP Differences: Europe vs. The World

Pinpointing precise country-by-country differences within Europe remains challenging due to potential data gaps; for instance, the reported number of German CDPs seems uncharacteristically low. However, clearer distinctions emerge when comparing the European CDP market to the global landscape.

Key Distinctions Between European and Global CDP Markets

- Campaign System Dominance: A striking 70% of European CDP employees work for companies offering campaign-type systems, which excel at selecting messages for individuals in both batch campaigns and one-on-one interactions. This contrasts with just 43% of employees in similar roles outside of Europe.

- Resource Efficiency: This strong preference for campaign systems among European marketers is likely influenced by fewer technical resources compared to their U.S. counterparts. Campaign systems offer a broader range of features, helping European marketers maximize their budgets and reduce the need for additional specialized products.

- Company Size and Funding: European CDP companies are generally smaller and less well-funded. On average, a European company has 59 employees and €6 million in funding, significantly less than the 99 employees and €25 million in funding typically seen elsewhere.

- Market Leadership: Only one of the top ten largest CDPs globally is based in Europe, whereas five of the ten smallest are European. This disparity is further emphasized by the age of these companies. Many large European CDPs (four out of six with over 100 employees) were founded before 2006, often starting as marketing services agencies before evolving into CDPs. In contrast, most large non-European CDPs were purpose-built as CDPs from their inception. (More details on non-European data can be found in the global industry update.)

Future Trends in the CDP Industry

Analyzing industry data assembled bi-annually by the Customer Data Platform Institute provides valuable insights into evolving trends.

- European Growth Slowdown: While the European CDP industry previously grew faster than the rest of the world, this trend has recently slowed, with Europe’s share of employment seeing a slight decrease.

- Shifting Vendor Focus: The clear historical shift from access vendors towards campaign vendors has also decelerated. Outside of Europe, this trend even reversed, with analytics vendors gaining market share. This suggests that different CDP types are successfully catering to diverse customer groups.

- Diverse Landscape Persistence: Contrary to many industries where a dominant model and a few leaders quickly emerge, the CDP industry is not expected to coalesce around a small number of vendors with similar features anytime soon.

- Declining Market Concentration: Data on industry concentration supports this, showing a steady decline in the share of employment among the top five vendors over the past two years. Even the share held by the top 20% of vendors (a number that naturally grows with the industry) decreased in the most recent period.

In conclusion, the European CDP industry remains vibrant and innovative, evolving with approaches tailored to its unique market conditions. While U.S.-based firms benefit from higher funding and a significant technical head start, they are particularly strong in the data access and analytics categories. This dynamic suggests a continued coexistence of both European and non-European vendors, often deployed for different strategic purposes within the same organization.